About those stupid 4-day workweek promises

The non-woke cultures just upped it to 6 days a week!

https://www.kedglobal.com/corporate-strategy/newsView/ked202401240001

GL

The non-woke cultures just upped it to 6 days a week!

https://www.kedglobal.com/corporate-strategy/newsView/ked202401240001

GL

https://europeanconservative.com/articles/democracy-watch/the-populist-revolt-europes-had-enough/

WOW

This is a great Piece

Democracy, as invented by the Ancient Athenians, had two constituent parts: demos–the people–and kratos–power or control. Since democracy re-emerged in its modern form in Europe, oligarchies have done all in their power to keep the demos and kratos as far apart as possible

It is time to go on the offensive and stand up for national democracy and sovereignty. Whenever they try to treat populism as a dirty word, I recall the definition of the p-word in the Cambridge Dictionary: “Populism—political ideas and activities that are intended to get the support of ordinary people by giving them what they want.” Giving the people what they want! Outrageous! That idea may fill the EU elites with horror. But we should surely embrace populism as another word for democracy.

Introducing the Hate Crime and Public Order Act has proved to be a disastrous move for Scottish First Minister and leader of the hard-left Scottish National Party (SNP), Humza Yousaf.

A large proportion of the first 4,000 hate crime complaints, submitted after the law came into effect at the beginning of this month, were rather humiliatingly directed at Yousaf himself. Polling released over the weekend also suggests that in the few weeks that the hate crime law has been in place, Yousaf’s popularity has plunged among Scots—including among SNP voters.

Findlay this week told his colleagues that the law “has transformed Scotland into a place of international mockery … where contentious discussions and disagreements in your own home can result in a knock at the door from the police. Where every single complaint, no matter how groundless or absurd, is subject to police investigation, while despairing officers are being told not to pursue real crimes.”

https://europeanconservative.com/articles/news/scottish-hate-crime-law-may-have-to-be-repealed/

THE CRETINS ARE LOSING THE SPORTS HEROS

TO A MAN , AND WOMAN ,THE TOP PLAYERS IN ALL SPORTS ARE GIVING CREDIT FOR THEIR SUCCESSES TO GOD…AND GOD IS THE CRETIN’S GREATEST ENEMY 🙂

https://jonrappoport.substack.com/p/scottie-scheffler-golfer-of-spiritual-ecstasy?

Thanks for these Charts Farmer…I have a different interpretation

A Cup and Handle Patter is Usually very Bullish

AND

Wedge Patters are Consolidation Patterns…they will always breakout one way or another

I see 4 reversal points so far thats an even number and therefore Bullish …and even if there is a pause at the top line..this being a log chart i bet that line is near 4,000

….

Rest my case

WOOO WHO !

April 18, 2024: Thanks to the tireless work of my esteemed colleague, James Roguski, and others, the WHO IHR (International Healthcare Regulations) are epically failing. James exposed how the negotiations between the Working Group (US, EU nations, NGO influence, et al) with 72 nations from the Africa Group and Group for Equity were quite contentious.

https://karenkingston.substack.com/p/biden-goes-directly-to-african-nations?

Ask your neighbour, friends, relatives, etc.

I haven’t asked lately but I would guess that PM’s and the miners are not on their radar screen.

As the modern version goes, when the person manning the Cell Phone Kiosk in the Mall gives you a hot tip on a miner, it’s possibly time to lighten up or plan your exit.

We are a long way from that point.

A former D.C. National Guard official is accusing two senior Army leaders of lying to Congress and participating in a secret attempt to rewrite the history of the military’s response to the Capitol riot.

In a 36-page memo, Col. Earl Matthews, who held high-level National Security Council and Pentagon roles during the Trump administration, slams the Pentagon’s inspector general for what he calls an error-riddled report that protects a top Army official who argued against sending the National Guard to the Capitol on Jan. 6, delaying the insurrection response for hours.

https://www.politico.com/news/2021/12/06/jan-6-generals-lied-ex-dc-guard-official-523777

Every year, researchers try to predict the four influenza strains that are most likely to be prevalent during the upcoming flu season. And every year, people line up to get their updated vaccine, hoping the researchers formulated the shot correctly.

The same is true of COVID vaccines, which have been reformulated to target sub-variants of the most prevalent strains circulating in the U.S.

This new strategy would eliminate the need to create all these different shots, because it targets a part of the viral genome that is common to all strains of a virus. The vaccine, how it works, and a demonstration of its efficacy in mice is described in a paper published today in the Proceedings of the National Academy of Sciences.

https://www.eurekalert.org/news-releases/1041168

https://www.pnas.org/doi/10.1073/pnas.2321170121

Fool me once shame on you – Fool me twice shame on me!

FROM Covid & Coffee — peer reviewed studies for future reference — because someday – someone at the tent (or family/acquaintances) might need to find this information:

He reported that just in the last two weeks, six new academic papers have been published linking covid mRNA vaccines to cancer, bringing the running total (by his count) to twenty-six. Here’s his list of the six new papers:

Hopefully this info helps somebody…………

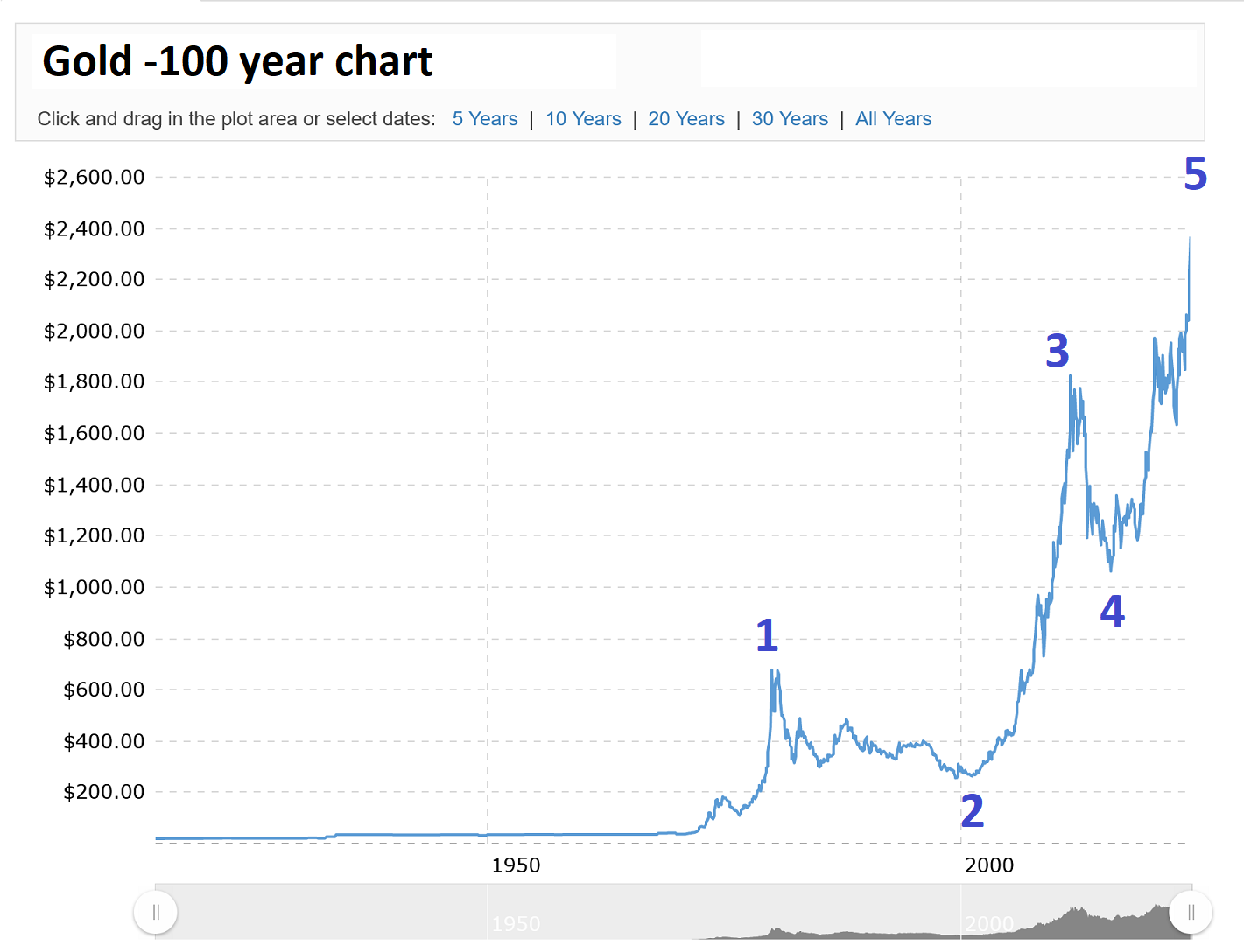

I will see your chart Fully and add two more to cap my point. Both are self explanatory but a few notes are added just in case. These charts come from Macrotrends and are shown on a one hundred year chart. Macrotrends offers its chart users the ability to look at the data in several ways. These include an inflation adjusted option and a logarithmic version. I have selected both options and presented charts here that I think reinforce what I am saying about gold. Namely, that gold is nearing highs from which it will soon retreat.

There is a price ceiling based on golds history. And these charts suggest where the next top will be located. Have a look. You may even come around to my point of view if you stare at these long enough. They are damning. Gold is going to have to put in a strong leap higher in order to break out of its channel and change the future. All things being equal and given that price behaves normally means gold will likely go back into a bear market in 2026.

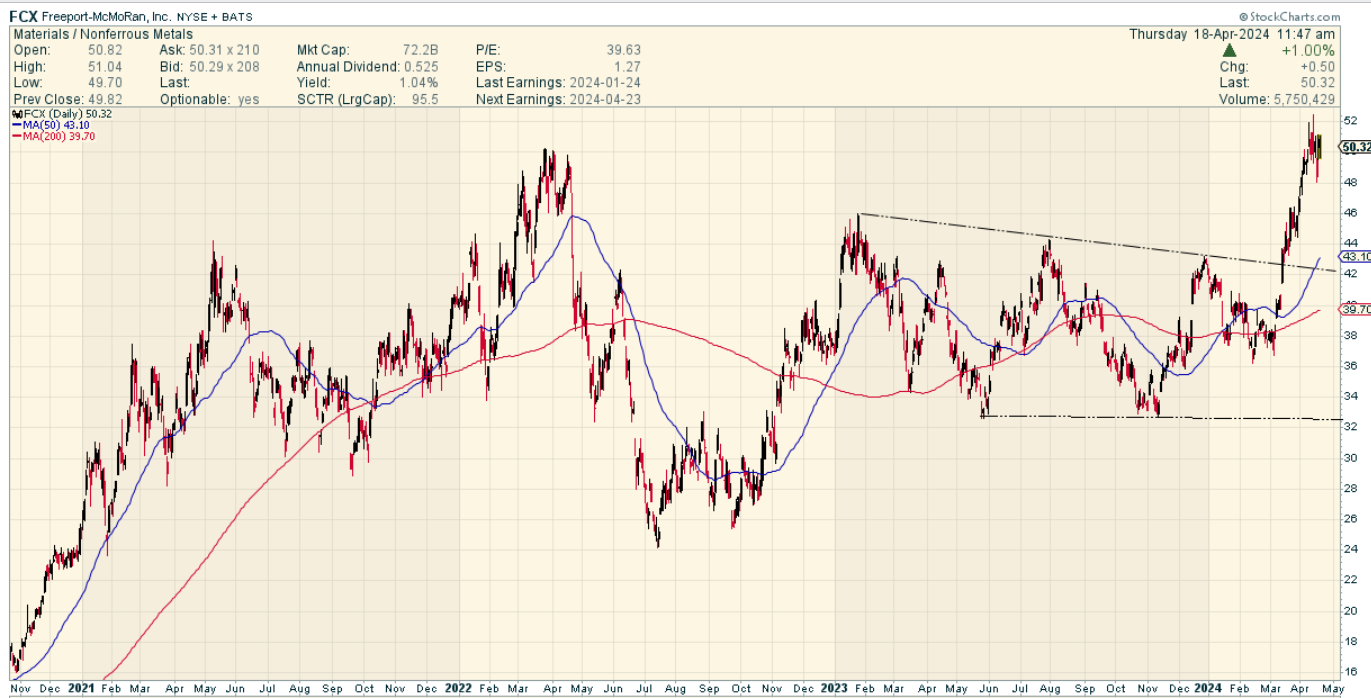

FREEPORT MAC

https://boriquagato.substack.com/p/the-road-back-from-serfdom

hint: cloaking devices

“if only there were a huge network, some sort of social media, owned by a guy with near infinite resources and a longstanding interest in privacy and payment systems.

if only that guy had ownership of not just to an internet network out of the reach of governments because it was in space, but had actual rockets to launch more and a US government dependency upon him for their own launches that makes him a bit untouchable.

hey, wait a minute…”

Holding on to the empire w/ Brian Berletic (Live)

Alex Christoforou, Alexander Mercouris, Brian Berletic (2:15:39)

https://www.youtube.com/watch?v=_Lvyfr-Fty0

Ukr Collapse: Rus Holds 40% Krasnogorovka, Storms Ocheretino, Ukr Mutinies; Israel Prepares Strike

Alexander Mercouris (1:18:55)

https://www.youtube.com/watch?v=8ZUKYGiyaTs

Hollywood fails to see Ukraine war can’t be won. Orban, EU leaders failed. Yolanda TIME Top 100

Alex Christoforou (33:40)

https://www.youtube.com/watch?v=K-n-seFCur8

MILITARY SUMMARY CHANNEL:

Complete Defeat In Ocheretyne | The Gloves Are Off. Military Summary And Analysis For 2024.04.18

Dima (8:01)

https://www.youtube.com/watch?v=aokDXvARFP0

The Turning Point | Ukrainian Armed Forces Entered The Donetsk Cauldron. Military Summary 2024.04.18

Dima (Live at 12:30 PDST, 15:30 EDST)

Anand, who is responsible for much of the public service, says all ministers will be expected to participate in the cost-cutting plan, not just the biggest departments.

The Federal Gov’t ADDED 27,000 employees last year — there are now 357,254 sucking at the gov’t teat — and they issue a PR to publicize a 5,000 decrease — which most likely will occur via normal annual staff attrition. 1% of employees = Scraping the barrel…….imo!

https://nationalpost.com/opinion/york-university-israel-support-racism

They are the teachers of our youth!

The Tytler Cycle (first time I’ve encountered this)

Similar to the Fourth Turning or the “Good times create weak men” cycle.

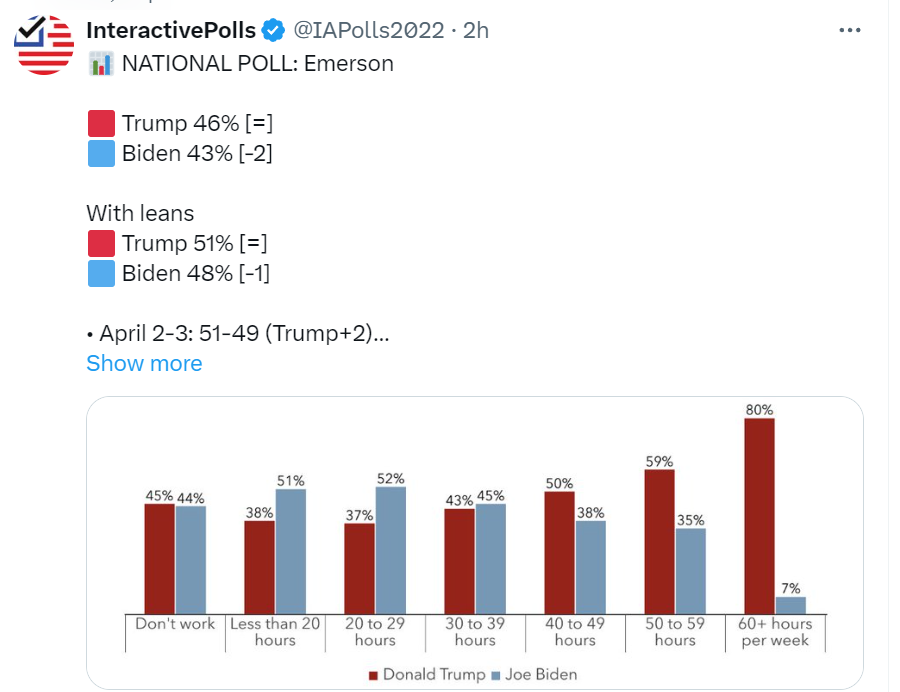

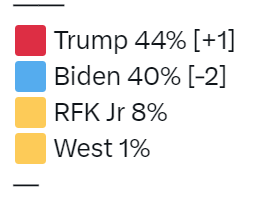

I’m a Poll Junky . I admit it. Some are Good . Some are bad . Some are Mundane .

Some are Inovative….They cross poll for Religious Affiliation , Race , Age , Income , Sex etc

THEN THERE’S THIS ! 🙂 KUDO’S TO EMERSON POLLING

Note according to Rich Baris (Polster Emeritus) Brandon needs about +4 in the Popular Vote to win the Electoral College

If you’re working More…You want Trump More 🙂

What about The Kennedy Effect ?

BUT WAIT…THERE’S MORE

ANOTHER INTERESTING TID BIT FROM THIS POLL

@ Farmer

I’ll see your chart and raise you one …Quarterly , Log Scale

click to enlight

“The American legal system deals with new technologies much as a reptile digests a meal–slowly. I get email from readers about defending the Constitution, something we all support. I am not an attorney, but my impression of Constitutional law is that it is a tediously complex thicket of case law that must be carefully picked through before we can even begin to understand exactly what we’re defending: every issue anyone might be concerned about has already accumulated an immense load of rulings and arguments.

This is American jurisprudence: advocacy goes to trial and ruling are issued, some as rulings that will pertain to all future cases and some that will not. The law advances in new fields such as AI as positions are argued before judges / juries and then reviewed by higher courts as losers appeal judgments / rulings.

…

AI has certain novel features which have yet to be decided by the processes of advocacy, rulings and appeals.”

http://charleshughsmith.blogspot.com/2024/04/the-spear-in-ais-back.html

“Now anti-trust regulators are finally looking at the uncompetitive wastelands created by Big Tech”

Here is a yearly chart of gold for you to examine. It is evidence (based upon a common technical approach) that gold has almost reached a top from which the only future movement will be price declines. Everything has a limit. Golds is at the 2.5 standard deviation mark of a yearly chart. That does not mean it cannot shoot higher and put in a spectacular year to finish up this cycle, but it does mean you should think twice before investing too heavily in the stuff because the technicals warn we are near a termination top.

Excellent analysis. https://www.americanthinker.com/articles/2024/04/the_robin_hood_effect.html

There will not be a lot of love for this post of mine. But I need to write this anyway since too many people have gone goofy over golds recent move yet very few of them have any background in the technical aspects of how price works. So I would like to push back against the euphoria by pointing out a few inconvenient truths.

In the chart below for example we can see that golds price is pretty clearly in a fifth wave move (Elliot) as it stands today. This is based on a hundred year chart. In fact no matter what historical chart we look at, gold is currently nearing the top of its upper range from where it will encounter serious resistance and go no further.

I am not putting a number on the actual final top in this post. Rather I just want to point out in general terms that we are nearer the top of a terminal upper range than a bottom and that structurally, golds upward advance in nominal terms is therefore fairly limited by the nature of its historical patterns.

The only gains possible beyond a certain point will be those acquired by outright currency devaluation. Since gold is priced in dollars it may seem obvious to some readers that a soaring gold price is guaranteed. But again, this whole idea of an imminent collapsing US Dollar is another faulty idea that is going to hit a brick wall soon for most people since it too is conjecture based and not well conceived.

For the moment, just keep in mind that gold is putting in a topping pattern now. Odds will soon favour a structural decline in the absence of a major dollar devaluation. So take care if you are betting the whole house on gold going to the moon and please do not fall for the snake oil sales pitches or allow yourself to be deluded by market prophets who are really no better than used car salesmen!

Multiple news articles but not a single one expressed an opinion on why he died?

Sad to see so many of our youth experiencing “suddenly & unexpected” deaths!!

One of the more difficult aspects of working in economic analysis is the problem of rampant disinformation that you have to dig through in order to get to the truth of any particular issue.

Establishment media sources lie incessantly about our financial conditions, and when they are finally cornered and forced to admit how bad things are, they then lie about the causes. That said, I find that these lies are usually designed to do one of two things: Over-complicate the problem so that people give up thinking about it, or, distract from the problem so that people blame a scapegoat.

https://twitter.com/RepMattGaetz/status/1780627938829848652

Wow….add this to other recent news / events unfolding in USA …. the Deagel forecast may prove accurate